For starters, I HATE the word Bollywood. It represents a stupidly-aping-the-west, we’ve-lost-our-narrative-roots version of the Hindi film industry.

While it was coined by the foreign press to negatively connote Hindi Cinema as a copy of Hollywood, we, like morons, have picked up that insult thrown at us and are wearing it like a badge of honour. Anyway… This post is not about that…

It’s about how there’s a serious business model problem in my Hindi Film Industry…

The Indian Film industry and the Hindi Film Industry

The Hindi Film industry is THE majority component of the Indian Film industry. It contributes almost 50% of the net domestic box office collections (BO) annually, despite comprising only 16% of the films made. The film industries of 13 other languages account for approximately 76% of the films that release but all-combined contribute only approximately 40% to the annual domestic box office collections. Hollywood/Int’l films are the balance.

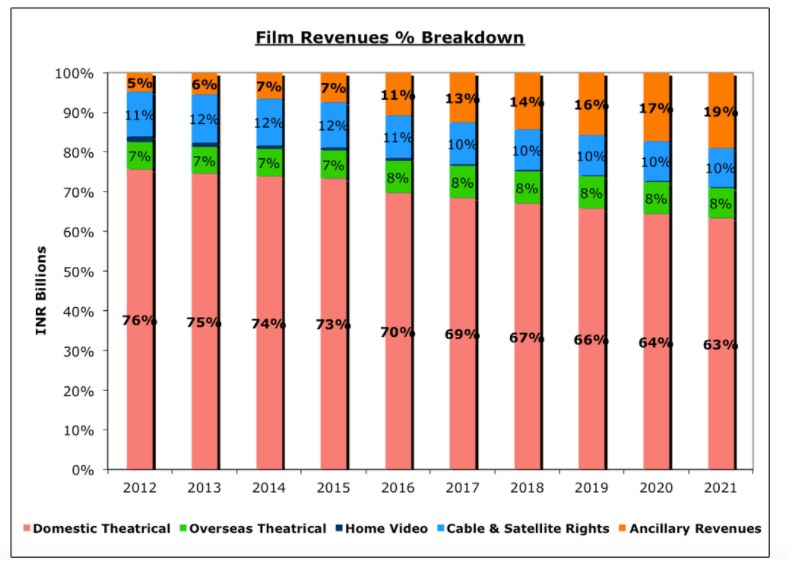

Further, the revenue breakup of the Film industry, is as under, where, in 2016, 70%+ revenues came from Domestic Theatrical and approximately 22% came from Cable and Satellite (C&S) + Ancillary (mostly digital) rights:

Fill Revenue Percentage Breakdown of the year 2016

So, if there is a major problem with the Hindi Films Domestic BO, it drags the whole industry down with it.

And there IS a MAJOR problem with Hindi!

The Viewership Problem

The Number of screens a film releases in and Average Ticket Price have both increased steadily over the past five years.

Yet, the no of Rs 100 crore plus films have remained around the same.

Films scoring Rs 100 Crore and Plus since 2012

Screens and ticket prices are increasing at a decent pace and the number of Rs 100 crore plus films are remaining around the same, this clearly indicates that the number of people buying tickets is dropping steadily each year. The same is also indicated through the occupancy/footfall numbers of Inox and PVR, as above…

There are multiple reasons for this.

Firstly, Hindi films simply aren’t able to keep up with the kind of content the urban under-20-yr-olds (U20s) of today watch and has caused them to lose a large chunk of these U20s as an audience. They watch Superwoman, TVF, Game of Thrones, Sherlock, Netflix and Hollywood. They find their ‘stars’ online. If you polled Urban-under-20s, Superwoman or PewDiePie or John Snow would probably be more popular than SRK. Hindi Films aren’t doing enough (if at all) to create the kind of content that this generation wants to watch/is currently watching.

India, the country, has had nearly 20 years of excellent growth (except for around 2008-10) and that growth has created a massive upper middle class, with significant disposable income. When people have disposable income, they spend it on education and they spend it on entertainment. When they are better educated, they are more world-aware. There is less cultural alienation from cultures (Hollywood/Europe) which are not their own and hence kids who have grown up in that period are as culturally comfortable watching international content as they are watching Indian content. So, Hindi Films now have serious competition from the high concept, high budget upscaled content that the US & Europe creates, and it is starting to show.

Secondly, Cinemas – India is one of the world’s most under-screened markets. At a cinema density of eight per million (as against USA of 125 per million), we are woefully short of screens. This puts pressure on the first weekend/week collections as films are likely to be replaced by newer films within one – two weeks. Leads to higher marketing costs. This means that all the resources of a producer / distributor are not utilised in making high quality content but instead in battling for mindspace in front of people. Further, this leaves no scope for word-of-mouth-publicity to kick in and leaves niche filmmakers in a lurch as ‘their’ audience may never get to watch the film in theatres.

This also puts extra pressure on the ticket rates as the revenue recoupment window for a film is one-two weeks at max. Increasing ticket rates have put the industry into a negative loop.

Also, a lot of the multiplex revenue comes from F&B which is dependent on footfalls. Lower footfalls means they have to increase rates to ridiculous levels. Today a PVR Phoenix Lower Parel sells samosas for Rs 80/-, the smallest popcorn they have is for Rs 180/- or 200/- and a chai for Rs 120/-. These markups are more than what a fine dining restaurant would charge. This ensures that film watching is even more expensive and hence even more prohibitive.

High ticket + F&B rates means fewer people can see films, which means that the industry needs to recover the same amount from fewer people hence they increase ticket rates even more which causes even fewer people to go for movies in the theatre…. and so on….

The Profitability Issue

Similar to the Hindi industry as a whole, the top 50 Hindi films too have shown no growth in BO collections. Despite increased screens and increased ticket rates, the collections of the top 50 Hindi Films have declined marginally each year for the past four yrs. So even the top 50 Hindi Films are losing audiences!

On top of that, there is a drastic reduction in profitability of these films. Box Office collections of the top 50 films have remained steady, but profitability has reduced to almost half.

Top 50 profitable Hindi films since 2012

Films are getting just too expensive. Whether it is inefficiencies arising from lack of planning (really unforgivable in this day and age) or it is greed at the top with star actors / directors asking for amounts which are way beyond what the financials of a film can reasonably afford or it is the crazy money spent on marketing; whatever may be the cause, the net impact is visible. Revenues aren’t growing in proportion to costs and profitability of the top 50 Hindi Films (really the cream of Hindi cinematic content) has significantly reduced in the past 5 years, from 60% to 36%.

We all get swayed by the 500%+ profit margin of a Baahubali / Dangal / Bajrangi Bhaijaan into thinking that the industry is doing well, without realising that these are the top 1% of Hindi films. So while a few (less than 25 films annually) create value for its investors, a massive majority of them destroy value.

Destruction of Value

Approximately 200 Hindi movies had a mainstream nation-wide theatrical release in 2016. The top 50 movies contributed around 96 per cent of the total box office, amounting to INR 25 billion (Rs 2500 Crores). The remaining 150 films had a cumulative BO of just INR 1 billion (Rs 100 Crores). That’s approximately Rs 67 lakhs per film (with only Rs 30 lakhs going to the distributor/producer). Average cost (including publicity) for these films would have been between Rs 4 crores – Rs 8 crores (Rs 6 crores on average). So that’s almost 900Cr of value destroyed by these bottom 150 films, in just 1 year.

Further, of the top 50 films, only 26 movies were able to earn more than Rs 30 crores each at the BO and that comprised around 80 per cent of the overall BO collection (approximately 2000 crores). So the the films ranked from 27-50 contributed only Rs 500 crores; an average of 20 crores per film (approximately Rs 10 crores going to the distributor/producer). Now, most of these films would have cost a minimum of Rs 30-40 crores (Rs 35 crores average). That means yet another Rs 400 crores of value destroyed by films comprising the bottom half of the top 50 films of 2016.

While some amount of this value is recouped through C&S rights, digital rights and music rights, that would not be more than 25% of the Rs 1300 cores + of value that these 175 films have destroyed in just one year.

Such large destruction of value both inhibits industry growth through internal accruals and makes it a less attractive destination for external funding. In a three-yr period where India has seen a record FDI inflow, external funding of the film industry has actually shrunk, with Disney not green-lighting any new films and Balaji moving their focus away from theatrical feature films to digital content. Old timers like Mukta Arts have diversified their focus too, with Education and Cinemas taking primacy over films.

This is worrying!

The Doomsday Forecast

If you walk into a multiplex cinema in Spain, France or Italy, nearly 75% of the shows are taken up by Hollywood films with less than 20% shows showing local content. Spain used to make almost 100+ films 20 years ago, today it makes less than 20. Same is the case with Italy. If the state would not have funded French films, the number would have been less than 10. Do note that these are countries that gave the world Almodovar, Goddard, Fellini, Truffaut, et al… But now the best French, Italian, Spanish, Australian, British talent is all working for Hollywood and is making very, very limited domestic cinema.

So, how has their domestic cinema disintegrated?

Hollywood has basically thrown great quality content at these countries and acquired market share. The citizens of these countries do not feel a cultural alienation against Hollywood content and are happy to watch it. Unable to create films that are good, are culturally global, travel well, and are well marketed globally, each of these industries has gotten into an internal negative loop and shrivelled up.

China, while being relatively isolated culturally from the ‘west’, has further protected its domestic industry from the Hollywood onslaught, by restricting the number of Hollywood Films that release.

The only two free markets that have successfully held back the Hollywood onslaught are India and the Latin American/South American industry. Apart from the language and cultural differences, both these industries have a long(er) cultural history than Hollywood does and its patrons have huge cohesion to domestic content.

However, with global awareness creeping into these markets via the internet, the next generation is no longer feeling that cohesion with local content and is happy to consume content from overseas, much like Spain, Italy and France.

My doomsday scenario is that 30 years from now, Hollywood / Netflix / Amazon will take over the content market share in India with 60% + market share, relegating the domestic industry to a distant 2nd with a market share % in the low 30s. I shudder when I think such thoughts and pray to The Force that this never happens.

The (Possible) Solution

They say a problem is a problem only if you have a solution. So there’s no point in writing about this problem if there isn’t a solution.

Short term solutions

(a) Pay cuts. The top of the cost pyramid of the industry has to take a pay-cut if this is to be a sustainable industry. If this destruction of value continues, we will see the investment by producers / studios slow down. We have already seen it with Disney and Balaji and some of the old-timers like the Sippys and Mukta Arts.

(b) De-grow the number of theatrically released films. Until multiplexes grow, we have to reduce the number of films releasing in theatres. We cannot have this crazy weekly onslaught of films at the BO which are unsustainable. Filmmakers have to use the TV / VOD / digital medium to distribute their films and hence make them in commensurate budgets. I am willing to bet that the reach & profitability of a film like ‘Lipstick Under My Burkha’ would be higher if it was made for the TV-VOD / Web-VOD market, with a slightly lower production cost & limited marketing cost. That would have enabled the producer(s) to distribute it online for a much lower cost than what people would have paid to watch it, in the 400-odd screens it released in. A low price point + word-of-mouth-publicity (WOMP) would have ended up with exponentially more viewers (hence more impact of the message the film needed to give) and definitely the same amount / more revenue than it received at the BO.

(c) Script is king, not star. We HAVE to make films where a ‘star’ is cast because the script demands it. Yes, the ability of a star to draw the audience in is definitely something that should be exploited to tell a good story and not be made the be-all & end-all of a film.

(d) Planning, efficiency, budget-consciousness. Short of creating an inhospitable work environment for the crew, the industry HAS to become crazily budget conscious and spend much more time in planning & pre-production than in principle photography. A ‘Jagga Jasoos’ taking four years to complete should simply be unacceptable.

Long-term solutions

EDUCATION – Teach students high quality filmmaking. Teach students their own domestic art, literature & culture so that they are able to tap into it for stories & inspiration. Also teach them international art literature & culture so that they are able to make films with global sensibilities which travel well. How Hollywood has de-alienated American culture for Indians, we need creators who will do the same for the world. And we need them here, making content in India. The government needs to get its act together by way of a formal film education policy framework (similar to Medical, Architecture, Law, CA), so that both private and government Film & Media schools can adopt it and the mainstreaming of Film & Media education happens.

CINEMAS – As mentioned earlier, India is one of the world’s most under-screened markets in the world. We need a serious push on screens. We need to double our multiplex screen count in the next 5 years. Possible only through government support by way of capital-expenditure incentives and tax holidays. More screens means films can play for longer without worrying about being taken off on account of the next ‘big film’. Longer playtime means distributors can stop worrying about the first weekend & hence spend less money on marketing the film to fill theatres in that first weekend. Longer runs for films means that niche / non-mainstream films that are discovered late (by word-of-mouth publicity) can still earn a decent profit. It also means that you have a scenario where the total money the makers of a very small niche film have can be the utilised towards its cost of production entirely and hence improve the production values of these films.

It has been 105 years since the first Indian film went into production. The steps we take over the next five years will determine what happens in the next 105…

The blog was originally published HERE

Categories: Recommended, View-point

Very well written Blog Chaitanya, i hope it reaches the core audience for whom this was meant for.

LikeLike